[ad_1]

If you take out a mortgage, whether or not it’s a refinance or a house buy, you could come throughout the phrase “money to shut.”

Just about all mortgages require some monetary contribution from the borrower to fund the mortgage.

It is perhaps down cost funds, it is perhaps lender charges, or it is perhaps pay as you go prices like property taxes and householders insurance coverage.

There’s probability it’ll be a mix of this stuff, which can have to be paid at closing by way of a verified account.

Let’s discuss extra concerning the that means of money to shut, the way it’s calculated, and the way it’s paid.

Money to Shut on a Residence Mortgage Is Extra Than Simply Closing Prices

If you happen to have a look at your paperwork, you must see an inventory of closing prices related to your own home mortgage.

You’ll be able to see estimates of those prices on each your preliminary Mortgage Estimate (LE) and likewise in your Closing Disclosure (CD).

And when it’s about time to shut your mortgage, on the settlement assertion ready by your escrow officer or actual property lawyer.

On these paperwork, you must see issues just like the mortgage origination price, underwriting and processing charges, and different lender charges.

Moreover, there’ll probably be a cost for an appraisal, together with a cost for title insurance coverage, householders insurance coverage, and escrow providers.

Below that escrow/title umbrella, extra charges might be listed, equivalent to courier charges, wire charges, notary charges, mortgage tie in charges, settlement charges, and on, and on.

There can even be recording charges and switch taxes, together with pay as you go gadgets equivalent to X variety of months of taxes or insurance coverage.

That’s the closing value piece, which incorporates each lender charges (if relevant), and third-party charges, such because the insurance coverage, appraisal, title/escrow.

Fairly easy, however we even have to contemplate the down cost, any deposit equivalent to earnest cash, and any vendor or lender credit.

Then some math must be executed to determine the ultimate quantity due, which is, drumroll, the money to shut.

Happily, there’s a piece on the LE and CD known as “Calculating Money to Shut,” which breaks all of it down for you.

How one can Calculate Money to Shut: An Instance

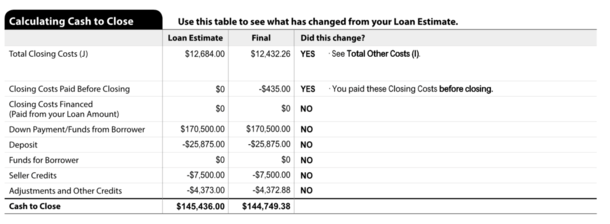

It’s in all probability simpler to take a look at an instance fairly than hold speaking about it. So try the screenshot above, taken from a Closing Disclosure.

As you’ll be able to see, it lists complete closing prices, down cost funds, deposits, and credit.

On this instance, the acquisition worth is $852,500 and the house purchaser is placing down 20% to keep away from mortgage insurance coverage and get a greater mortgage charge.

They’ve bought $12,432.26 in closing prices, of which $435 was paid out-of-pocket earlier than closing for an appraisal.

The borrower made a $25,875 earnest cash deposit for 3% of the acquisition worth as properly, which was initially $862,500 earlier than a slight worth discount.

They didn’t finance any closing prices, nor did they obtain any funds by way of the transaction.

However they did get a vendor credit score of $7,500 and a $4,372.88 rebate from their actual property agent.

So to tally it up, we’ve got $182,932.26 in complete prices, and $38,182.88 in credit.

Which means the borrower nonetheless owes $144,749.38, which is the remaining steadiness after their deposit and varied credit.

It covers the remaining down cost and remaining closing prices, and is usually wired to escrow at closing.

What About Money to the Borrower?

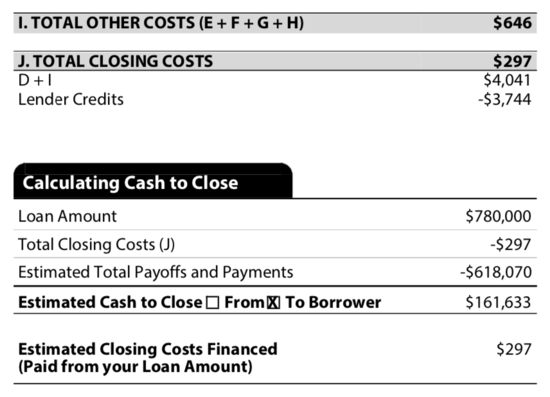

Now let’s have a look at a money out refinance. On this case, there’s money going to the borrower at closing as a result of they’re tapping their house fairness.

So as an alternative of sending cash to the lender, the financial institution is sending cash to the borrower.

On this instance, the borrower additionally took benefit of a lender credit score, which offset almost all of their closing prices.

Their mortgage payoff on their present mortgage was $618,070 and the brand new mortgage quantity was $780,000.

That might ship $161,930 to the borrower, however as soon as we subtract the $297 in remaining closing prices, it’s $161,633.

Sending the Money to Shut: Some Issues to Keep in mind

When it comes time to ship your money to shut funds, you’ll probably accomplish that by way of wire, or presumably a cashier’s verify.

Both means, the funds should come from a sourced account that was verified through the underwriting course of.

For instance, a checking account you verified earlier on by connecting it within the digital utility or importing month-to-month statements.

This fashion they know the cash is definitely coming your personal funds, and never another unverified supply.

If it does come from a non-sourced account, it might delay your mortgage closing and trigger loads of complications.

Keep in mind, such funds also needs to be seasoned for a minimum of two months prior as properly, that means within the account and untouched for 60+ days.

Once more, this ensures the funds are your personal and never another person’s, or worse, a mortgage, which you deposited into your personal account.

When you have questions on what’s owed, it’s at all times useful to talk instantly with the settlement officer, who can go over all the things with you line by line.

That means you already know precisely what you owe, why you owe it, and most significantly, the place precisely to ship it.

To summarize, there are loads of prices related to a house mortgage, a lot of which you received’t pay attention to till you undergo the method your self.

For this reason it’s crucial to get a sturdy mortgage pre-approval and put aside funds properly earlier than starting your own home search.

[ad_2]