[ad_1]

On a day when mortgage charges are formally near hitting 8%, I made a decision to put in writing a put up about why they may be rather a lot decrease in 2024.

Name me a contrarian. Or an optimist. Or maybe simply a person that’s taking a look at information and drawing some conclusions.

Whereas the development for mortgage charges these days has undoubtedly been larger, larger, larger, we might be near hitting a peak. I do know, I’ve stated that earlier than…a lot for the mortgage price plunge.

However possibly we simply must cross that psychological 8% threshold earlier than issues can turnaround.

Generally you might want to see/expertise the worst earlier than a restoration can happen.

Right here Come the 8% Mortgage Charges…

The specter of 8% mortgage charges may last more than the 8% mortgage charges themselves, assuming they really materialize.

This isn’t a brand new risk. I wrote all the best way again in September 2022 to be careful for 8% mortgage charges. At the moment, we inched nearer to these ranges earlier than charges pulled again.

Extra lately, Shark Tank’s Mr. Fantastic referred to as for a similar, arguing that the Fed wasn’t messing round when it got here to its inflation battle.

And now it seems he may be proper, with the 30-year mounted averaging 7.92%, no less than by MND’s every day survey.

However regardless of larger and better mortgage charges over the previous month and a half, the Fed has develop into an increasing number of dovish.

There have numerous feedback of late from Fed audio system primarily signaling a pause in price hikes. Mainly arguing that no additional tightening is important.

That doesn’t imply 10-year bond yields can’t hold rising, nor does it imply mortgage charges can’t additionally enhance.

Whereas the Fed is saying one factor, everybody else is wanting on the information, which continues to come back in hotter than anticipated.

About 10 days in the past, it was a giant jobs report print, and at the moment it was retail gross sales coming in a lot larger than forecast.

Per the Commerce Division, retail gross sales elevated 0.7% in September, greater than double the 0.3% Dow Jones estimate.

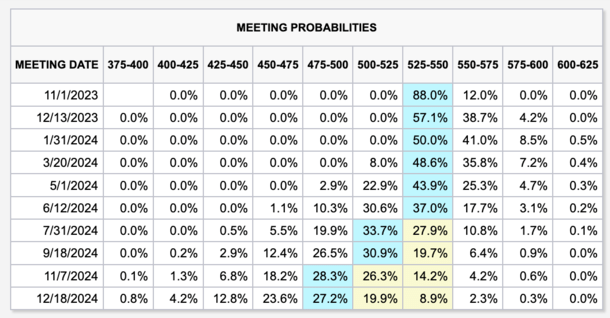

This has pushed the percentages of one other Fed price hike up for the December assembly to close parity with a pause.

Per the CME FedWatch Software, probabilities of a price hike on the December thirteenth assembly are actually at 41.9%. That’s up from 32.7% yesterday and 25% per week in the past.

Ought to We Hearken to the Fed or the Knowledge?

It’s been a wierd distinction these days, with the Fed changing into extra dovish as scorching information continues to come back down the pipe.

However in the end it seems as if the rate of interest merchants are extra targeted on the information than they’re what Fed audio system need to say.

Even so, the percentages stay ever so barely in favor of a pause, which is nice information in the intervening time.

After all, these numbers can change shortly, as evidenced within the every day and weekly motion highlighted above.

And if shoppers hold spending, regardless of financial headwinds and better costs, it may be tough to see the cooler financial stories the Fed desires.

Nonetheless, the Fed should still stand pat at these ranges and look forward to situations to deteriorate, as can be anticipated after 11 price hikes.

Right this moment, Richmond Fed President Thomas Barkin stated the new information “doesn’t match together with his on-the-ground observations that demand appears to be slowing.”

So maybe we simply want extra time to let the restrictive financial coverage do its factor. It’s not as if shoppers instantly cease spending simply because prices are larger.

Individuals nonetheless want to purchase issues, particularly fuel, groceries, clothes, and different necessities.

And because of all of the credit score floating round, whether or not it’s 0% APR credit playing cards or purchase now, pay later platforms, the celebration can proceed for lots longer.

The ten-12 months Yield Is Forecast to Fall in 2024, Pushing Mortgage Charges Down with It

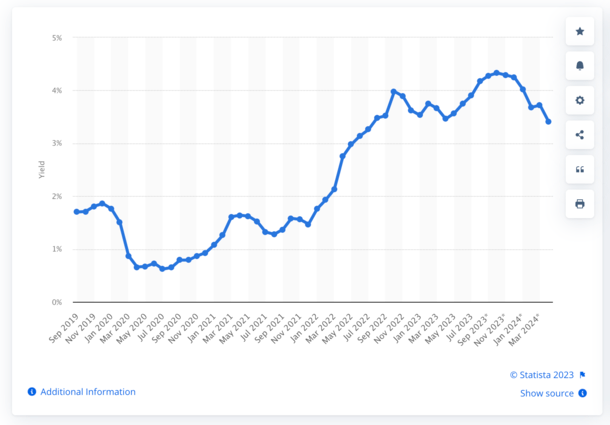

Eventually look, the 10-year bond yield, which tracks 30-year mounted mortgage charges fairly properly, was a sky-high 4.86%.

In the meantime, the mortgage price unfold was over 300 foundation factors, when it’s usually nearer to 170.

Mixed, meaning a yield of 5% would sign 8% mortgage charges. In regular occasions, it might translate to a price of say 6.75%. However these should not regular occasions.

This explains why mortgage charges hold rising, as mortgage lenders are going to proceed to cost defensively if the specter of extra inflation and price hikes stays.

However possibly, simply possibly, we’re approaching the worst of it, as shoppers teeter getting ready to a potential recession.

And maybe the 8% mortgage charges will sign a peak and potential turning level.

In spite of everything, the 10-year treasury yield is predicted to fall to three.41% by April 2024, per a September twenty seventh word from Statista.

Sure, such forecasts are topic to alter, however the basic consensus is that we’ll be decrease by mid-2024. Simply possibly not that low.

But when we take a decrease 10-year yield and sprinkle in a extra conventional mortgage price unfold, say simply 200 foundation factors, that places mortgage charges again within the 6% vary.

Mortgage charges within the 6s, and even high-5s if paying low cost factors at closing, would usher in some normalcy to the housing market.

If accompanied by a light recession and a few job losses, it may additionally imply barely decrease house costs as properly, as a substitute of a return to bidding wars.

And that might be good for the long-term well being of the housing market, which is clearly damaged proper now.

(photograph: Eli Duke)

[ad_2]