[ad_1]

How does an extra $1 trillion in annual dwelling mortgage origination quantity sound?

For the time being, it sounds unimaginable should you’re within the mortgage business and struggling to drum up enterprise.

Quantity has plummeted over the previous 12 months due to sky-high mortgage charges and an absence of for-sale stock.

However that would change if rates of interest creep again down and stock begins to rise once more.

Even when circumstances don’t enhance all that a lot, FICO rating competitor VantageScore believes the implementation of their credit score scoring mannequin might assist tremendously.

FICO Scores Are the Solely Sport in City, However That Will Quickly Change

For the time being, mortgage lenders rely solely on FICO scores to find out a borrower’s creditworthiness.

These scores vary from 300 to 850, with scores beneath 620 thought of subprime.

Come 2024, a brand new credit score rating supplier will be part of the fray, no less than for loans backed by Fannie Mae and Freddie Mac.

The Federal Housing Finance Company (FHFA), which oversees Fannie and Freddie, introduced earlier this 12 months that the implementation of the brand new credit score rating fashions is predicted to roll out over two phases in 2024 and 2025.

Within the third quarter, they anticipate the supply and disclosure of extra credit score scores offered by VantageScore. And the substitute of FICO legacy scores with the brand new 10T mannequin.

By the fourth quarter of 2025, it will embrace the incorporation of the brand new scores into pricing, capital, and different processes.

Together with that, they’re transitioning from requiring three credit score reviews (generally known as a “tri-merge”) to requiring simply two credit score reviews (“bi-merge”).

So debtors with credit score scores from simply two of the three main credit score bureaus may have much less concern qualifying for a mortgage.

And it might be cheaper to buy a bi-merge credit score report as a substitute of a tri-merge report.

However the greatest potential influence is in permitting a totally new credit score rating supplier into the mortgage area.

Mortgage Lenders Might Originate 2.7 Million Extra Dwelling Loans

VantageScore believes it could actually broaden homeownership as a result of its credit score rating incorporates many extra credit-invisible debtors.

Their analysis discovered that hundreds of thousands of customers characterised as “dormant” are merely rare or uncommon customers of credit score.

They cite an instance would possibly of a shopper who prefers to pay in money however just lately repaid an auto mortgage with out lacking a cost.

Whereas these customers might not have FICO scores, they could possibly be scored with VantageScore.

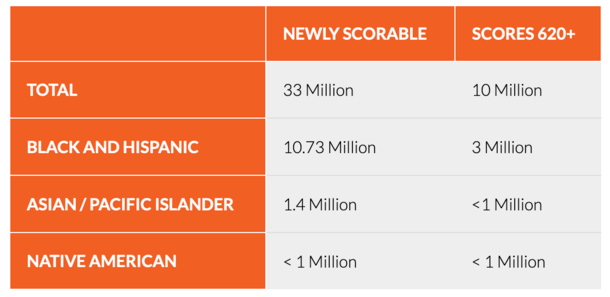

The corporate says such customers accounted for 73% of the newly scoreable inhabitants and 91% of the newly scoreable inhabitants with credit score scores over 620.

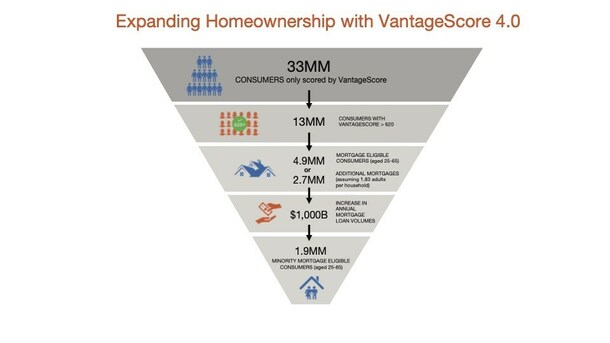

In complete, VantageScore estimates that 33 million customers can solely be scored by them.

Of these, some 13 million have a VantageScore of over 620, which as acknowledged is the subprime cutoff.

It’s additionally the bottom credit score rating accepted by Fannie Mae and Freddie Mac for a conforming mortgage.

They additional break it right down to 4.9 million mortgage-eligible customers aged 25 to 65 and estimate that there are about 1.83 adults per family.

This might end in 2.7 million extra mortgages, leading to an extra $1 trillion in annual mortgage origination quantity.

And 1.9 million minority mortgage-eligible customers, which is a giant focus for the GSEs and particular person banks and lenders.

The mathematics works out to a mean mortgage quantity of roughly $370,000. It’s a giant quantity, however even when a few of their declare materializes, it could possibly be a giant shot within the arm for the mortgage business.

What About Mortgage Default Charges and VantageScore?

You may be questioning if utilizing a brand new, comparatively unparalleled credit score rating is a good suggestion within the mortgage area.

Particularly at a time when housing affordability has not often been worse. It’s a respectable query.

Whereas this has definitely been an apparent concern, the corporate claims default charges for customers “had been higher or just like these of customers conventionally scored.”

That is based mostly on “rigorous testing carried out throughout mannequin growth and on an ongoing foundation.”

However finally, we received’t know for positive till these credit score scores are literally put to the take a look at.

Both method, one might argue that permitting various scores from a number of distributors is sweet for avoiding monopolies.

By the best way, VantageScore was developed by the nation’s three Nationwide Shopper Reporting Businesses (NCRAs), Equifax, Experian, and TransUnion.

It was launched in 2006, and has taken practically 20 years to get this level. So it’s going to absolutely be a giant deal as soon as carried out.

Their latest mannequin scores roughly 94% of all adults 18 and older, “with out sacrificing security and soundness.”

This consists of traditionally marginalized, minority, and lower-to-middle earnings Individuals.

The corporate mentioned greater than 3,000 lenders used greater than 19 billion VantageScore credit score scores in 2022, a 30% improve from 2021.

[ad_2]