[ad_1]

Whereas forecasters usually disagree concerning the anticipated path of financial coverage, the extent of disagreement as measured within the New York Fed’s Survey of Major Sellers (SPD) has elevated considerably since 2022. As an illustration, the dispersion of expectations concerning the future path of the goal federal funds fee (FFR) has widened considerably. What explains the present elevated disagreement in FFR forecasts?

One attainable cause is that sellers’ coverage fee forecasts are based mostly on projections for different variables, resembling inflation and unemployment, and their expectations for these variables have diverged. One other chance is that the disagreement is about the way in which wherein these macroeconomic variables have an effect on the coverage fee—the perceived “response perform” of the policymaker. On this publish, we examine which is a greater description of the information. Our outcomes level towards the previous rationalization: Permitting macroeconomic outlooks to fluctuate throughout SPD respondents, whereas protecting the coefficients of the perceived response perform fixed, is healthier at accounting for the widened cross part of coverage fee forecasts.

Disagreement concerning the Future Path of Financial Coverage Has Elevated

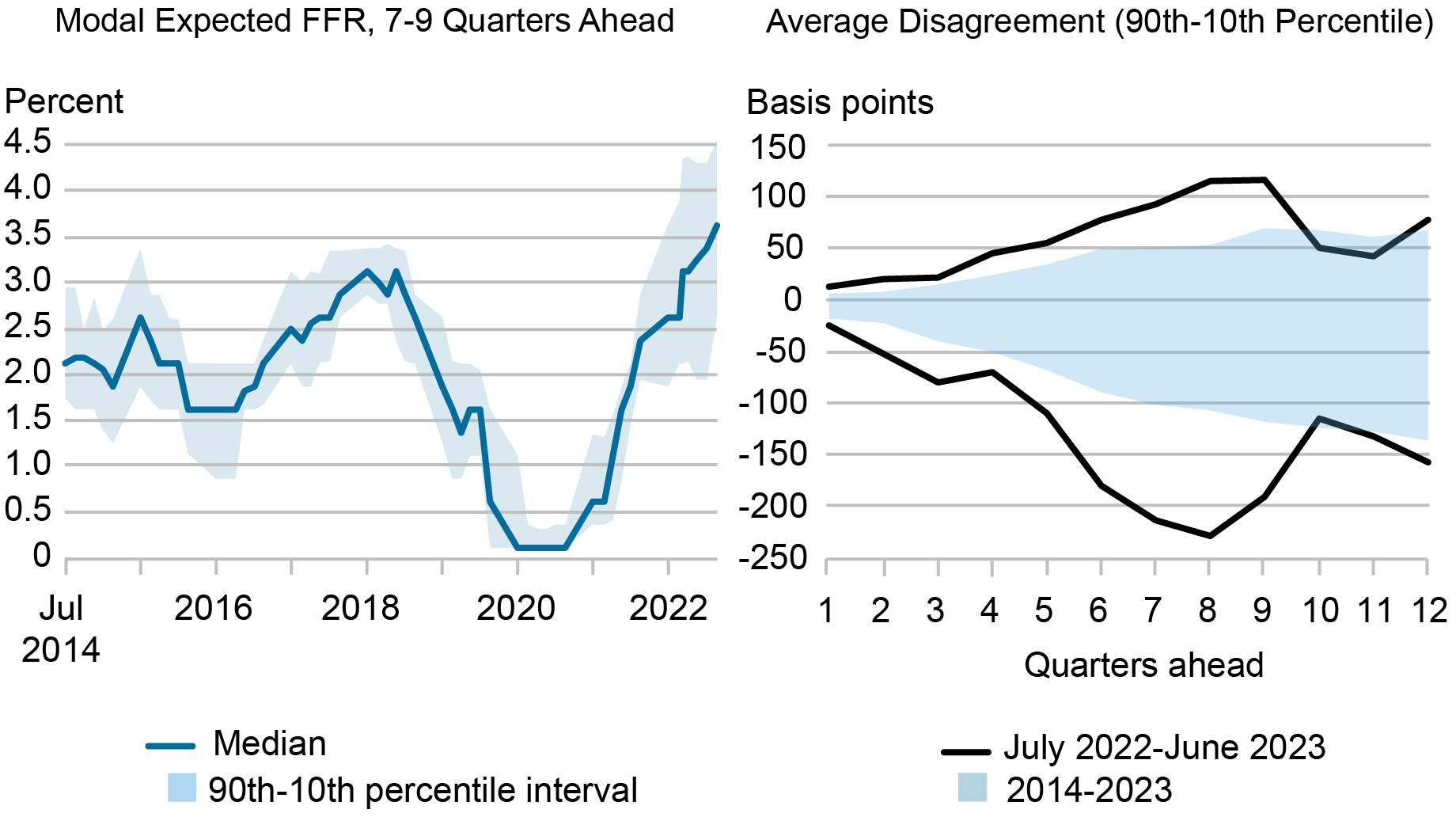

The dispersion of sellers’ expectations concerning the future path of the coverage fee has widened considerably in current surveys. The left panel of the chart beneath exhibits the extent and vary of expectations for the goal FFR seven to 9 quarters forward, utilizing information from the SPD. The blue stable line is the median FFR expectation throughout respondents, and the shaded areas illustrate the space between the Ninetieth and Tenth percentiles. Whereas dispersion fell in the course of the pandemic in 2020-21, as sellers anticipated close-to-zero coverage charges for a while, since 2022 it has elevated to over 2 proportion factors, essentially the most in ten years.

Dispersion of Expectations Has Widened

Sources: Authors’ calculations; Survey of Major Sellers.

Notes: The left panel reviews the median (line) and Ninetieth-Tenth percentile vary (shaded space) throughout survey respondents of the modal coverage fee expectation seven, eight, or 9 quarters forward, by survey date. The information are from the Survey of Major Sellers spanning the interval July 2014–June 2023. FFR is federal funds fee. The correct panel reviews the imply distance between the Ninetieth and Tenth percentiles, by variety of quarters forward, for the total pattern (shaded space) and for the current pattern (black traces).

The correct panel of the chart highlights the extent of disagreement relative to its historic norm, and exhibits that over the previous 12 months it has been pronounced throughout a number of horizons. For expectations eight quarters forward collected since July 2022, the Ninetieth and Tenth percentiles have been on common 3.5 proportion factors aside, or greater than twice the space within the historic pattern.

Disentangling Variations in Financial Outlooks vs. Perceptions of Financial Coverage Guidelines

In our evaluation, we assume that survey respondents implicitly use a Taylor rule in forming coverage fee expectations. In essence, we posit that the anticipated coverage fee for a given horizon is the same as the sum of its long-run anticipated worth and the contributions of core PCE (private consumption expenditures) inflation and unemployment, for that very same horizon, weighted by their respective response perform parameters. We re-estimate the response perform parameters over time, permitting for modifications in respondents’ perceptions, however these parameters are assumed to be uniform throughout horizons (three to 12 quarters forward) inside a survey pattern. To strike a steadiness between time variation and pattern measurement, we use rolling samples that embody three surveys every.

Our method follows an unlimited educational literature that employs linear regressions to estimate Taylor rule–like financial coverage guidelines; see, as an illustration, Bernanke (2015), Carvalho and Nechio (2014), and Bauer, Pflueger, and Sunderam (2022). It’s essential to notice that, due to the inherent codependence of anticipated coverage charges and anticipated macroeconomic outlooks, linear regression estimates needs to be interpreted because the co-movement perceived by forecasters between the coverage fee and the macroeconomic variables thought-about, reasonably than as causal relationships. That mentioned, regardless of the endogeneity drawback, Carvalho, Nechio, and Tristão (2021) discover assist for utilizing strange regressions.

To gauge whether or not differing macroeconomic outlooks or coverage rule perceptions higher account for the noticed dispersion in FFR expectations, we conduct two empirical experiments.

Experiment #1: Frequent Coverage Guidelines, Various Financial Outlooks (CR-VO): We estimate the widespread set of Taylor rule parameters that most closely fits the panel information (the pooled estimation), after which we use the dealer-specific expectations for inflation and unemployment (together with the person long-run expectations) to foretell coverage fee expectations. This experiment solutions the counterfactual query: What would the cross part of sellers’ expectations be if all of them used the identical Taylor rule parameters however not the identical macroeconomic outlooks?

Experiment #2: Various Coverage Guidelines, Frequent Financial Outlooks (VR-CO): We estimate the set of Taylor rule parameters that most closely fits every particular person seller’s information, after which, holding these estimated particular person coverage rule parameters fixed, we impose widespread (median) expectations for inflation and unemployment throughout respondents. This experiment solutions the counterfactual query: What would sellers’ expectations be if all of them agreed on their macro expectations however had totally different views concerning the coverage rule?

The closest precedent to those experiments is Carlstrom and Jacobson (2015), though their evaluation depends on information from the Survey of Skilled Forecasters from 1995-2008.

Sellers Agree on the Coverage Rule, Disagree on the Financial Outlook

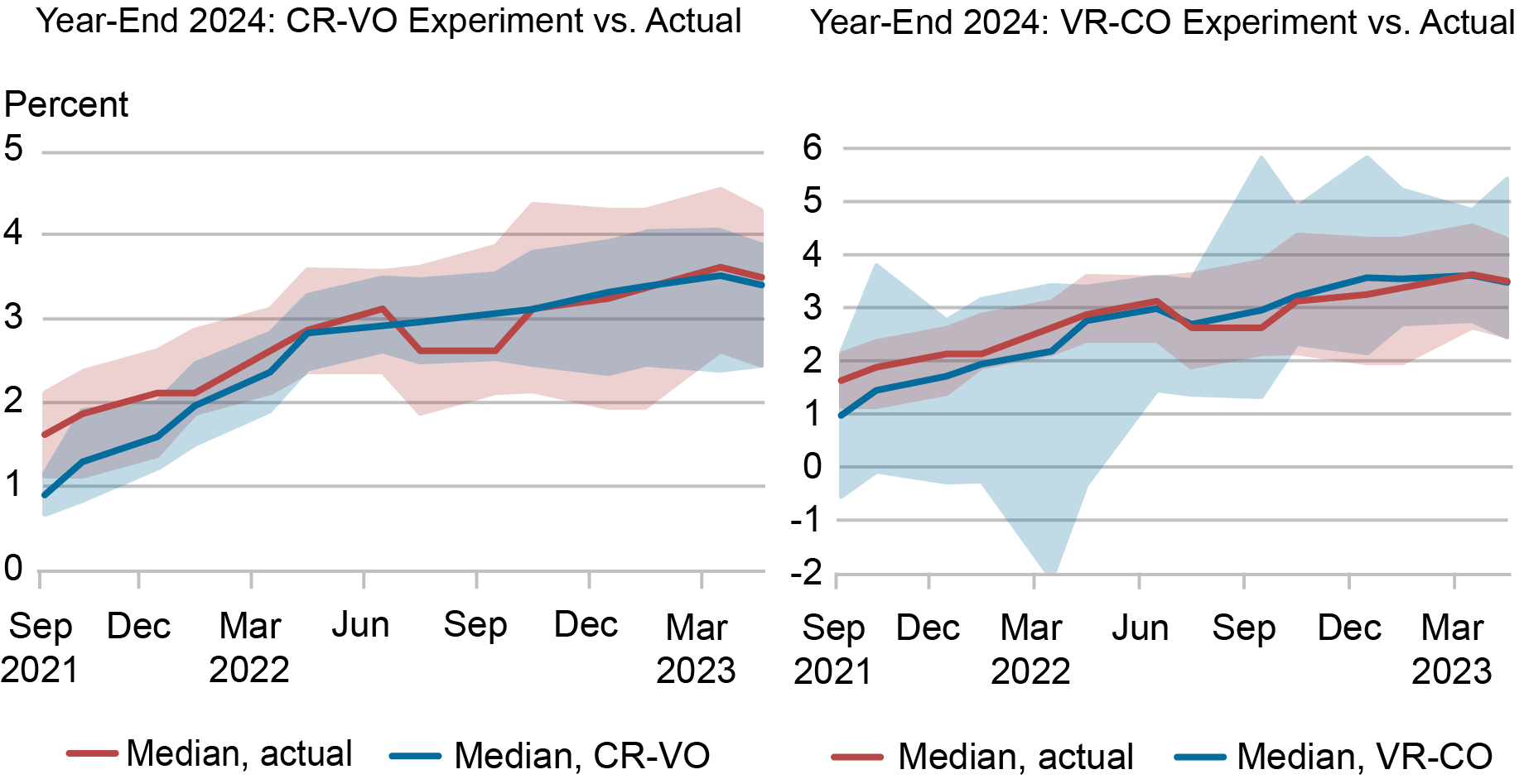

Since we’re particularly within the current improve in disagreement, we give attention to the forecasts for year-end 2023 and 2024, as reported by surveys carried out since July 2020. We present year-end 2024 forecasts within the chart beneath. In each panels, the purple stable line and shaded area present the noticed median expectations and the Ninetieth–Tenth percentile band. The blue stable line and shaded areas present the corresponding percentiles for the 2 experiments.

CR-VO Experiment Higher Matches Precise Forecast Distributions

Sources: Authors’ calculations; Survey of Major Sellers.

Observe: The panels present the precise and predicted distributions (Tenth, fiftieth, Ninetieth percentiles) below the assumptions of fixed parameters and ranging outlooks (CR-VO) throughout survey respondents, versus fixed outlooks and ranging parameters (VR-CO), for year-end 2024.

The chart illustrates the central findings. The dispersion of coverage fee expectations implied by experiment CR-VO higher overlaps with the dispersion of precise forecasts. The dispersion of expectations implied by experiment VR-CO, alternatively, is normally a lot bigger than the dispersion of noticed expectations. Thus, the counterfactual situation wherein sellers maintain a standard view concerning the policymaker’s response perform however disagree on the financial outlook suits the noticed information higher than the choice. We observe the same sample when year-end 2023 forecasts.

To some extent, this discovering is no surprise, as dealer-specific response perform parameters are estimated from small samples and due to this fact one would count on the cross-sectional dispersion to be huge. Nonetheless, the expectations fitted by experiment VR-CO are unable to match the elevated disagreement that we observe in precise expectations in current instances.

Contemplate once more the chart above: whereas the precise Ninetieth–Tenth percentile vary of the coverage fee will increase from 1 proportion level to 2.4 proportion factors between January 2022 and December 2022 (when peak disagreement is reached), disagreement assuming uniform macro outlooks (and ranging response perform parameters) will increase marginally, from 3.5 proportion factors to three.7 proportion factors, whereas disagreement assuming uniform response parameters (and ranging outlooks) rises from 1 proportion level to 1.6 proportion factors.

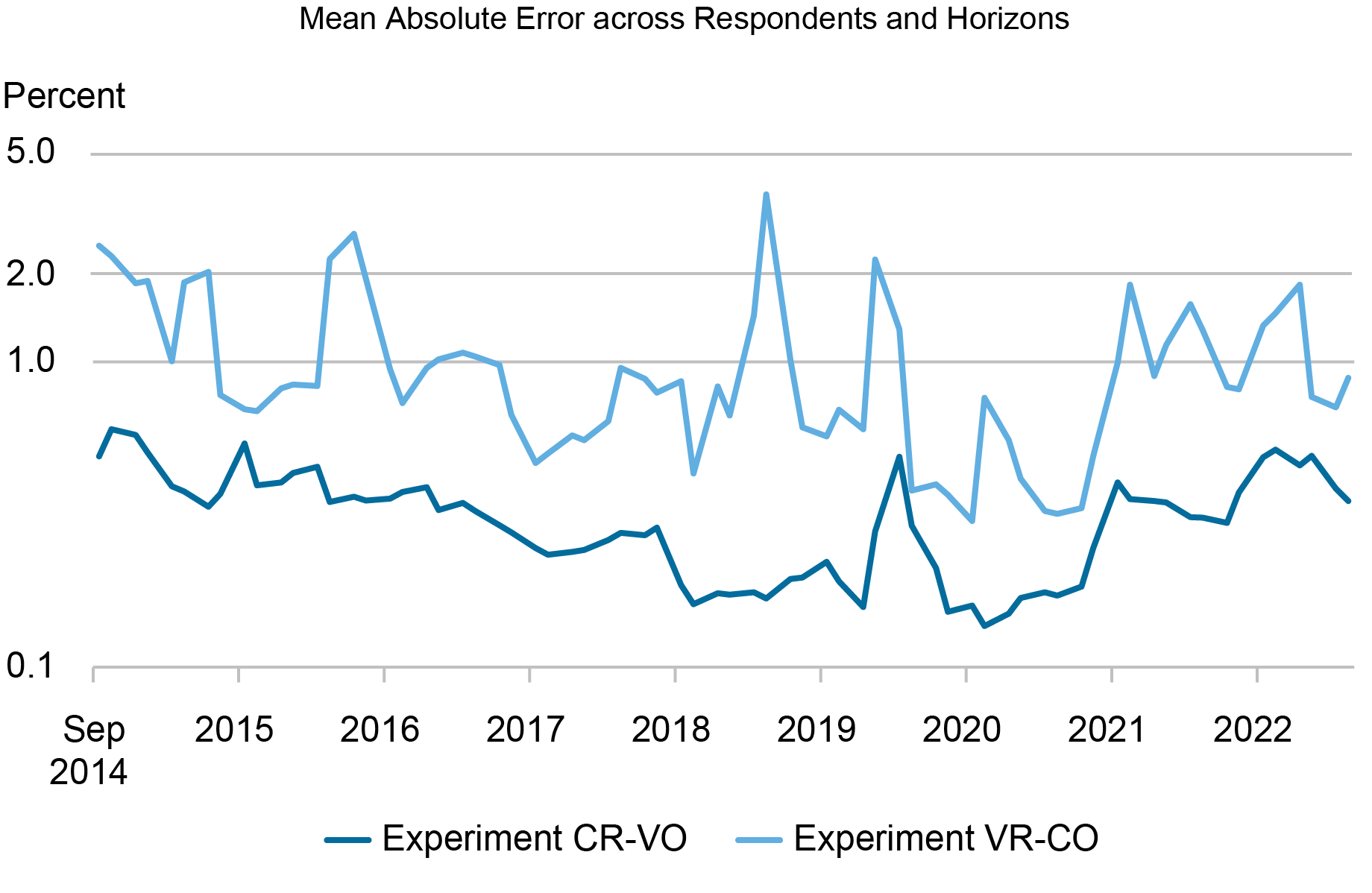

To quantify the relative match of the widespread coverage rule versus widespread financial outlook explanations, the chart beneath exhibits the imply absolute error (MAE) of experiments CR-VO and VR-CO, pooled throughout respondents and horizons, for every survey.

Imply Absolute Error Is Decrease for CR-VO Experiment

Sources: Authors’ calculations; Survey of Major Sellers.

Notes: The chart reviews the imply absolute error between precise forecasts and the fitted forecasts, for every survey date, produced assuming widespread coefficients and ranging outlooks (CR-VO) and assuming various coefficients and customary outlooks (VR-CO). The y-axis is in logarithmic scale.

A decrease MAE implies a better-fitting mannequin, which is the case for the sequence computed for the experiment with widespread coverage guidelines and ranging outlooks for each survey in our pattern. The typical errors produced by experiment CR-VO are smaller than these for VR-CO by a big margin (discover the log scale). In current months, the relative and absolute MAEs of the 2 experiments are roughly throughout the historic norm. As well as, be aware that each sequence improve in periods related to coverage uncertainty: the beginning of the 2020 pandemic and within the current interval of elevated inflation. Nonetheless, the swings within the MAE implied by the common-outlooks experiment are bigger.

Conclusion

Sellers’ expectations for the financial coverage path have diverged in current instances. Given uncertainty about how the Federal Open Market Committee (FOMC) would reply to a traditionally uncommon mixture of persistently excessive inflation and low unemployment, one would possibly count on sellers’ disagreement to stem not less than partly from divergent views on the Federal Reserve’s response perform. We discover, nevertheless, that it’s the financial outlook that accounts for the lion’s share of the elevated disagreement.

On the time the analysis on this publish was carried out, Arunima Sinha was an affiliate professor of economics at Fordham College and a visiting scholar within the Federal Reserve Financial institution of New York’s Markets Group.

Giorgio Topa is an financial analysis advisor in Labor and Product Market Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Francisco Torralba is a coverage and market evaluation principal within the Federal Reserve Financial institution of New York’s Markets Group.

Find out how to cite this publish:

Arunima Sinha, Giorgio Topa, and Francisco Torralba, “Why Do Forecasters Disagree about Their Financial Coverage Expectations?,” Federal Reserve Financial institution of New York Liberty Road Economics, August 2, 2023, https://libertystreeteconomics.newyorkfed.org/2023/08/why-do-forecasters-disagree-about-their-monetary-policy-expectations/.

Disclaimer

The views expressed on this publish are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).

[ad_2]