[ad_1]

Within the face of continued claims inflation, new knowledge from Client Intelligence reveals the house insurance coverage market could possibly be making strikes to guard itself.

The price of building supplies has seen a major improve since 2021 following a collection of financial elements. Pile on will increase in labour prices in addition to provide points for key constructing supplies like concrete and metal, and it’s no marvel dwelling insurers are going through substantial uplifts in the price of claims and repairs.

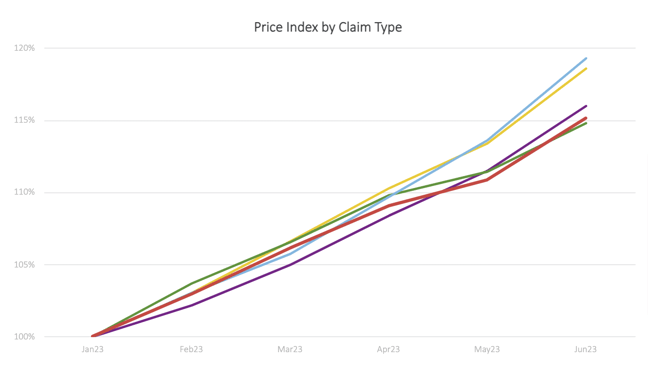

In response to a report revealed by Go.Examine earlier this yr, water and injury claims had been the most typical declare kind for the house sector in 2022. Within the first half of 2023, water and injury claimants confronted greater premium inflation, when in comparison with different sorts of claimants and people with no claims.

Escape of water claims incurred a median improve of 19.3% over the six-month interval and injury claims noticed an 18.6% improve. In distinction, premiums rose 16% for constructing claimants, 14.8% for theft claimants and 15.1% for non-claimants.

While the distinction could appear marginal between these two teams once we have a look at the trended view, we are able to see a transparent divergence emerge in April 2023 and proceed via to June 2023 – presumably an indication of the market responding to the earlier yr’s claims knowledge in an effort to guard mixed working ratios.

SOURCE: CI MARKET VIEW (PCW PRICE BENCHMARKING). SAMPLE SIZE: 2100 RISKS RUN EACH MONTH PER PCW.

|

Declare Sort |

YTD inflation |

|

Escape of Water |

+19.3% |

|

Harm |

+18.6% |

|

Constructing |

+16.0% |

|

No Claims |

+15.1% |

|

Theft |

+14.8% |

This isn’t the one transfer we’ve seen throughout the market. Some manufacturers look like steering away from claimants by quoting much less. In June 2023, 14 manufacturers quoted for a smaller proportion of claimants than non-claimants, by at the least 10% – together with two manufacturers not quoting for claimants in any respect.

Once we have a look at the manufacturers best for claimants, 5 out of 6 inflated premiums extra for claimants in comparison with non-claimants – clearly demonstrating the house markets transfer to guard itself in opposition to claims inflation.

[ad_2]