[ad_1]

Asset Location

A typical actual property mantra is “location, location, location.” Whereas some are unaware and others don’t think about it, location issues to traders, too.

On the subject of investing, there are two varieties of diversification:

- Asset diversification

- Asset location

You diversify your belongings by holding several types of belongings. This implies holding shares and bonds. It contains holding U.S.- and non-U.S.-based belongings. It additionally entails holding belongings of assorted sizes and with totally different aims.

To the extent doable, you additionally need to have a distinct kind of diversification. You need to maintain your belongings in several types of accounts from a tax perspective. That’s what asset location is all about.

Asset location refers to what kind of account an funding is held in from a tax perspective. You may maintain investments in tax-deferred accounts (e.g., Particular person Retirement Accounts or IRAs), taxable accounts, or tax-exempt accounts (e.g., Roth IRAs). You may also maintain them in Well being Financial savings Accounts, which offer a triple-tax profit. Being attentive to asset location can enhance your portfolio’s after-tax returns. For each further greenback your portfolio earns, it can save you one greenback much less – or spend one greenback extra later.

Traders extra generally concentrate on asset allocation and/or diversification. Many research present the way in which you diversify your belongings throughout totally different asset lessons drives your funding returns. Asset allocation additionally helps scale back threat. In brief, we don’t need to “put all our eggs in a single basket.” If we diversify, we will enhance the chance of reaching our long-term objectives. We will additionally improve our potential to comprehend long-term features.

Account vs Holistic

Many advisors handle portfolios and implement monetary plans on the account degree. This implies they handle every account individually reasonably than taking a collective view. Account-level administration sometimes places a full allocation of investments into every account. Consequently, shoppers with a 60/40 asset allocation mannequin have the identical investments in the identical percentages in every of their accounts, i.e., taxable accounts, IRAs, Roth IRAs, and so forth.

This method makes it a lot simpler to handle a consumer’s belongings. But it surely has some disadvantages for shoppers who maintain belongings in each taxable and tax-deferred accounts. Failing to find particular funding varieties amongst account varieties can scale back the tax effectivity of your portfolio. For instance, when shopping for or promoting a brand new safety, you might purchase or promote it in every account. If selecting what belongings to carry in a 401(ok) account with restricted choices, you will have to pick an inferior alternative to take care of the specified diversification parameters. Failure to concentrate to asset location may enhance your total tax invoice.

At Apprise, asset location issues. It is a crucial consideration for each consumer. For some shoppers, asset location shouldn’t be doable initially. Why? They maintain all their retirement belongings in a office 401k. If that’s the case, we search for alternatives to begin a Roth IRA, a taxable brokerage account, or a Well being Financial savings Account.

Sadly, we can’t make a definitive rating of the kind of investments to put in tax-deferred accounts. Why? A number of changeable components can impression such rating:

- Tax charges. – These can change because of the political surroundings in addition to an investor’s earnings degree.

- Funding Holding Intervals. – These may be particular to the investor and the technique she implements.

- Return Parameters. – These are continuously in flux as they’re affected by the economic system in addition to market efficiency.

Elements Affecting Asset Location

It’s best to think about the next components when deciding the kind the place to find an funding.

- Are you able to place the funding in a tax-deferred account? Sadly, you can not personal all funding varieties in tax-deferred accounts. For instance, below the tax code, you can not personal collectibles in IRAs. There are some exceptions associated to valuable metals, together with sure gold and silver cash issued after 1986, together with silver, platinum, and palladium bullion.

- Taxation of Curiosity. Whereas there are some exceptions (e.g., municipal bond earnings), most curiosity is taxable as atypical earnings.

- Taxation of Capital Positive factors. You understand a capital acquire whenever you promote or alternate an funding for greater than the acquisition worth. Brief-term capital features get taxed as atypical earnings. They come up whenever you promote investments held for a yr or much less. Lengthy-term capital features consequence from the sale of an asset held for a couple of yr. The tax charge for long-term capital features is decrease than the investor’s atypical earnings tax charge.

- Taxation of Capital Losses. You understand a capital loss whenever you promote or alternate an funding for lower than its price foundation. In taxable accounts, capital losses offset any capital first. Brief-term features and losses get mixed, leaving you with a internet acquire or loss. Then you definately comply with the identical course of for long-term features and losses. If capital losses exceed features, you may deduct as much as $3,000 of such losses yearly. You may carry unused capital losses till used. Producing a capital loss in a tax-deferred account supplies no tax advantages.

- Taxation of Dividends. Certified dividends are paid out of company earnings and obtain the identical preferential tax charge as long-term capital features. However not all dividends are certified. For a dividend to be certified, it should have been paid by a U.S. company or a certified overseas company. You need to additionally personal the inventory for greater than 60 days throughout the 121-day interval that begins 60 days earlier than the inventory’s ex-dividend date. Dividends from tax-exempt firms or organizations that typically should not topic to earnings tax are non-qualified. They typically get taxed on the similar charge as atypical earnings. (See beneath for particular guidelines associated to dividends paid by Actual Property Funding Trusts – REITs.)

- International Taxes Paid. For those who personal non-U.S.-based securities, you might pay withholding tax on any dividends you obtain. For those who maintain the shares in a taxable account, you may declare both a credit score (dollar-for-dollar discount in taxes) or a deduction for the withholding tax whenever you file your tax return. Please observe that solely earnings taxes, which embody withholding taxes, qualify for credit score in your U.S. tax return.

- Dividends Paid by Actual Property Funding Trusts (REITs). REIT dividends are thought of pass-through earnings to the shareholder. This permits them to qualify for the certified enterprise earnings or QBI deduction. This deduction was created as a part of the Tax Cuts and Jobs Act of 2017. It went into impact within the 2018 tax yr. The QBI deduction means that you can deduct the lesser of: 20% of your certified enterprise earnings (QBI), plus 20% of certified actual property funding belief (REIT) dividends, and certified publicly traded partnership (PTP) earnings, or 20% of your taxable earnings minus internet capital acquire.

- Tax-Deferred Accounts. Tax-deferred accounts enable a taxpayer to delay paying taxes on belongings contributed to the account till some future date – sometimes when the belongings are withdrawn. Examples of tax-deferred retirement financial savings accounts embody 401(ok), 457, and 403(b) plans for workers in addition to Keogh plans for self-employed people. These plans mean you can contribute a proportion of your pre-tax wage into a number of funding accounts. This supplies tax-free progress. Common or conventional IRAs are additionally tax-deferred accounts.

- Tax-Deferred Belongings. Tax-deferred belongings enable a taxpayer to defer at the least a number of the earnings the asset generates.

- U.S. Financial savings Bonds. Homeowners of U.S. financial savings bonds can wait to pay taxes till they money within the bond, when the bond matures, or after they switch the bond to a different proprietor.

- Grasp Restricted Partnerships (MLPs). For those who personal shares of a grasp restricted partnership, you may benefit from the tax deferral embedded inside its construction. MLPs can use depreciation to offset distributed money flows. This causes the taxable quantity they distribute to unitholders to be decrease than the precise money distribution. Untaxed distributions may lead to a discount in your foundation within the shares. (This implies you scale back what you paid for the shares by the quantity of this distribution. Consequently, whenever you promote shares of an MLP at a acquire, a number of the features might be taxed on the decrease capital features charge.

- Tax-Exempt Standing. Tax-exempt refers to earnings earned or transactions which can be free from taxation. Examples of tax-exempt retirement accounts embody Roth 401(ok), Roth 403(b), and Roth IRA accounts. You fund such accounts with after-tax {dollars}. These present future advantages. Withdrawals taken following a five-year interval after contributions to the account have been made, and usually, after the account proprietor is at the least age 59 ½, should not topic to taxes.

- State and Native Taxes. Some securities are exempt from federal and/or state taxes.

- Municipal Bonds. Curiosity earnings obtained from investing in municipal bonds is free from federal earnings taxes. Usually, curiosity earnings traders obtain from securities issued by municipalities inside their state of residence can be exempt from state and native taxes. Curiosity earnings from bonds issued by U.S. territories and possessions is exempt from federal, state, and native earnings taxes in all 50 states.

- Curiosity Revenue from Treasury Payments and U.S. Financial savings Bonds. You pay federal earnings taxes on curiosity earnings earned from Treasury payments, notes, and bonds. However you don’t pay state and native earnings taxes on such quantities. Equally, you pay federal earnings tax on earnings from U.S. financial savings bonds. You don’t pay taxes on this earnings on the state or native degree.

Different Tax-Exempt Accounts:

- 529 Faculty Financial savings Plans. The 529 financial savings plan can be a tax-exempt account. You contribute after-tax {dollars} to the account. Nonetheless, you pay no taxes on portfolio earnings supplied you utilize the funds for academic functions. Many states additionally enable taxpayers to deduct contributions to such accounts.

- Well being Financial savings Accounts (HSAs). You may make tax-deductible contributions to HSAs. You may withdraw quantities that reimburse certified medical bills tax-free as effectively. Belongings held in such accounts may typically develop tax-free.

Some Benefits of Asset Location

It’s best to attempt to maintain tax-inefficient investments in retirement accounts, tax-efficient investments in taxable accounts, and high-return investments in Roth IRAs. Why? Appreciating investments held in an IRA will get taxed at atypical earnings charges upon withdrawal. This therapy will even apply to your heirs.

If held in a taxable account, appreciation in your belongings doesn’t get taxed until and till you promote the asset. In that state of affairs, capital features tax charges, that are decrease than atypical earnings tax charges, apply. Subsequently, holding appreciating investments in retirement accounts is like telling the federal government it’s okay to doubtlessly pay rather more in taxes.

One other benefit: In case you are a long-term buy-and-hold investor and don’t have to promote appreciated belongings held in taxable accounts throughout retirement, your heirs will profit. Underneath present legislation, the premise in such belongings will get stepped as much as truthful market worth whenever you die. Your beneficiaries may doubtlessly pay no tax in any respect when promoting the asset.

Holding tax-inefficient investments, similar to U.S. bonds, in a retirement account, successfully defers any taxes till you begin drawing down the account. Though this may lead to atypical tax when earnings are realized, the earnings would have been topic to atypical tax anyway. Whilst you can maintain municipal bonds in a taxable account, they nonetheless sometimes present much less earnings. Additionally, fixed-income investments have a tendency to supply decrease long-term returns than equities, leading to decrease required minimal distributions and fewer potential for earnings inclusion whenever you move belongings on to your heirs.

Holding the very best return investments in a Roth IRA ensures the best tax effectivity from an account that will by no means be topic to tax. Which means the account ought to solely maintain equities. Whereas it will possibly entail extra threat, it is best to have a very long time horizon for a Roth account. That makes it higher suited to deal with unstable investments with the potential to supply larger long-term returns.

Having investments with higher progress potential in a Roth account supplies two main advantages.

- You don’t pay taxes in your features.

- Your heirs gained’t pay taxes on withdrawals from Roth accounts both. (Word that heirs, aside from your partner, will typically solely have 10 years to withdraw cash from a Roth IRA.)

There may be one different issue to think about. For those who promote investments held in retirement accounts at a loss, you’ll not understand such losses for tax functions. Not each funding will go up in worth; some are certain to say no.

Examples Exhibiting the Advantages of Asset Location

Curiosity Revenue: Assume your goal asset allocation is 70% equities and 30% mounted earnings. If you do not want present earnings out of your portfolio, asset location can show useful. How? Maintain any fixed-income securities in your IRA. Why? You gained’t pay taxes on the curiosity earnings they generate. Word that this issues rather less in at this time’s low-interest-rate surroundings

Fastened-income belongings are much less possible to supply significant progress. That results in a second profit. If you withdraw cash out of your account, your tax invoice might be much less. Keep in mind that withdrawals out of your IRA get handled as atypical earnings. Abnormal tax charges are larger than capital acquire charges.

Please don’t interpret any of this as which means we don’t need to see your belongings develop. We do. That’s at all times one in every of our aims after we handle a consumer’s portfolio. Asset location pertains to deciding which belongings you maintain in every account kind. If in case you have a couple of account kind, you need to take into consideration which kind of asset belongs through which kind of account.

International Taxes: You’re a shareholder of a French company. You obtain a $100 refund of the tax paid to France by the company on the earnings distributed to you as a dividend. The French authorities imposes a 15% withholding tax ($15) in your dividend earnings. You obtain a verify for $85. You report the $100 as dividend earnings. The $15 of tax withheld represents a certified overseas tax. You may declare the $15 of overseas taxes as a credit score towards the taxes owed in your dividend earnings. Which means your tax invoice might be decrease.

You possibly can deduct the overseas taxes as an alternative, however that’s normally much less favorable than a tax credit score. You need to itemize any overseas taxes you deduct. You additionally should deduct all of your overseas taxes. You can not take a credit score for some and deduct others.

However you may’t deduct overseas taxes you pay on investments held in a tax-deferred retirement account. The earnings in these accounts shouldn’t be topic to present U.S. tax (at the least not till you start making withdrawals).

However don’t fear—you gained’t lose the advantage of the overseas taxes you paid in these accounts. The overseas taxes scale back the earnings earned in that account. It’s such as you take a deduction towards the earnings, and whenever you withdraw the cash, you’re solely taxed on the web quantity. It’s like claiming an itemized deduction to your overseas taxes.

If in case you have a Roth IRA, the state of affairs is a bit totally different. Withdrawals from Roth accounts should not taxed by the IRS, so the overseas taxes you paid present no advantages. However don’t let the absence of a tax profit deter you from holding overseas investments in your Roth account. In some circumstances, it may nonetheless make sense to have overseas belongings in these accounts. There are numerous different components to think about aside from taxes when making funding selections. For instance, portfolio diversification and the suitability of the asset to your portfolio.

Appreciated Belongings: You purchased 200 shares of XYZ Inc. for $10/share. Twenty years later the shares are value $150 every. Pat your self on the again for deciding to purchase these shares. You turned a $2,000 funding into $30,000. Assume you’re within the 15% tax bracket for capital features. You file a joint tax return, and your earnings is $200,000 in retirement. Good job. You probably did an important job of saving for retirement, too. Your submitting standing is Married Submitting Collectively. Let’s take a look at the distinction in tax price whenever you promote the shares and withdraw the web proceeds. Word: This evaluation excludes state earnings tax results:

- Shares held in a taxable account: You will have a capital acquire of $28,000 ($30,000 – $2,000. With a 15% tax charge, you pay $4,200 ($28,000 x 15%) of federal earnings taxes. Your internet proceeds: $25,800 ($30,000 – $4,200).

- Shares held in your IRA: For this goal, your acquire or loss doesn’t matter. You apply your 24% tax charge to the $30,000 of gross sales proceeds. You pay $7,200 in taxes ($30,000 x 24%). Your internet proceeds: $22,800 ($30,000 – $7,200).

- Shares held in your Roth IRA or HSA: Your acquire or loss doesn’t matter for this goal both. You pay no taxes whenever you withdraw the gross sales proceeds. (Assume you’ve got certified medical bills if withdrawing funds out of your HSA.) Your internet proceeds: $30,000 ($30,000 – $0).

These tax financial savings matter. They turn into much more significant whenever you apply them throughout a complete portfolio.

Don’t Let the Tax Tail Wag the Canine

Limiting the quantity of taxes you pay is a correct method so long as it maximizes after-tax returns. That’s the profit tax location methods can present. Nonetheless, bear in mind to not make selections solely based mostly on tax implications. Plus, to implement such a method, portfolios have to be managed on the family degree and never on an account-by-account foundation. This may add complexity. It may well additionally make the returns in particular person accounts uneven. Total, using such a method can mean you can profit from decrease present and future taxes.

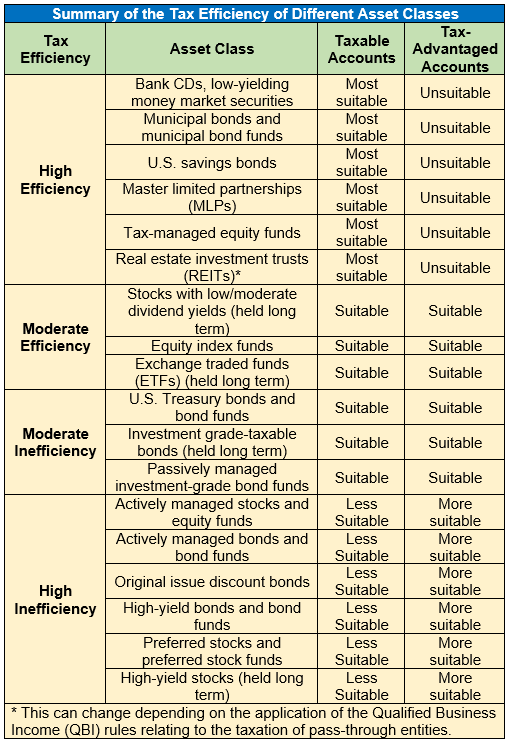

Asset Location Abstract: Tax Effectivity of Completely different Asset Courses

Tax-inefficient investments sometimes embody these offering a excessive anticipated return that’s within the type of present earnings. Investments with the best potential tax legal responsibility are those who needs to be prioritized when contemplating tax-advantaged accounts.

Traders must also concentrate on the tax advantages related to sure securities. For instance, municipal bonds, U.S. authorities securities, and MLPs present tax advantages that make them extra acceptable for taxable accounts.

Abstract

Contemplating which account ought to maintain which investments issues. It may well assist traders with each taxable and tax-advantaged accounts scale back their taxes. It typically helps to seek the advice of with an expert earlier than making asset location selections. Strategies on this weblog could not apply to everybody as its main goal is offering normal steerage.

Concerning the Creator

Phil Weiss based Apprise Wealth Administration. He began his monetary companies profession in 1987 working as a tax skilled for Deloitte & Touche. For the previous 25 years, he has labored extensively within the areas of non-public finance and funding administration. Phil is each a CFA charterholder and a CPA.

Do you know XYPN advisors present digital companies? They will work with shoppers in any state! Discover an Advisor.

[ad_2]